Important: This guide is for general education and planning awareness only. It does not constitute financial, legal, tax, CPF, banking, valuation, investment or property advice. Always verify your situation with the relevant authorities, your bank, lawyer, tax adviser and qualified professionals before committing.

What Own-Stay Buyers Should Understand First

A private property bought for own stay should not be assessed the same way as a pure investment property. Rental yield and resale profit may still matter, but the first question is whether the home fits your family, lifestyle, budget, cashflow and long-term holding power.

The real question is not “Can I buy?”

The better question is: after downpayment, stamp duties, CPF usage, loan servicing, renovation, monthly expenses and emergency reserves, can you live in the property comfortably without becoming over-stretched?

Three Core Areas Every Private Buyer Should Review

1. Budget

Your budget is not only the purchase price. It includes cash outlay, CPF usage, loan size, BSD, possible ABSD, legal fees, renovation, furnishing, maintenance and emergency funds.

2. Unit Selection

Floor level, facing, layout, afternoon sun, noise, privacy, lift access, stack position and future family needs can affect daily living more than many buyers realise.

3. Pricing

A good unit is not automatically a good buy at any price. Buyers should compare recent transactions, nearby alternatives, project attributes and total ownership cost.

The Private Buyer Own-Stay Framework

Financial Readiness

Check income stability, cash savings, CPF OA, loan eligibility, TDSR, LTV, BSD, possible ABSD and emergency reserves.

Family Fit

Review number of bedrooms, work-from-home needs, school access, elderly parents, children, pets, parking and future lifestyle changes.

Location Utility

Consider commute, MRT access, expressways, schools, groceries, healthcare, parks, family support and neighbourhood maturity.

Project Quality

Study developer track record, maintenance profile, unit mix, facilities, site layout, parking, density and management expectations.

Unit Selection

Assess layout efficiency, natural light, ventilation, privacy, views, west sun, noise exposure, wasted space and future usability.

Exit Flexibility

Even for own stay, buyers should consider future saleability, rental demand, nearby supply and whether the home remains relevant over time.

Budget: What Buyers Must Count Before Committing

Many buyers focus on monthly instalments, but private property ownership has both upfront and recurring costs. A responsible budget should include enough buffer for both expected and unexpected costs.

Upfront Costs

- Option fee or booking fee

- Downpayment

- Buyer’s Stamp Duty

- Possible Additional Buyer’s Stamp Duty

- Legal and conveyancing fees

- Valuation, bank and administrative fees where applicable

- Renovation, furnishing and moving costs

Ongoing Costs

- Monthly mortgage instalment

- Condominium maintenance fees

- Property tax

- Utilities and home insurance

- Repairs and replacement costs

- Higher cash outlay if CPF contributions reduce later

- Emergency reserve for income disruption

Start with the Property Affordability Calculator Singapore before shortlisting units.

Loan, CPF and Stamp Duty Checks

Total Debt Servicing Ratio

Private property buyers should understand how their total monthly debt obligations affect borrowing capacity. Car loans, credit cards, personal loans and other debt commitments can reduce affordability.

Loan-to-Value

LTV can be affected by outstanding housing loans, loan tenure, borrower age and lender assessment. A buyer may qualify for less loan than expected.

CPF Usage

CPF Ordinary Account savings may be used for eligible residential property purchases in Singapore, subject to CPF rules and limits.

Buyer caution: Passing loan assessment does not automatically mean the purchase is comfortable. Buyers should also stress-test interest rates, cash reserves, family commitments and longer-term income stability.

New Launch or Resale Private Property?

Own-stay buyers should compare both new launch and resale options carefully. The best choice depends on timeline, budget, urgency, location, unit size, renovation needs and risk comfort.

New Launch

- Progressive payment structure

- Newer facilities and fresh lease

- More unit choices at early launch phases

- Waiting period before key collection

- Need to review floor plans, site plan and showflat information carefully

- Future supply and completion timing matter

Resale Private Property

- Can physically inspect the actual unit

- Immediate or shorter occupation timeline

- May offer larger layouts in older projects

- Renovation and repair costs may be higher

- Need to check maintenance condition and MCST matters

- Lease age and future saleability should be reviewed

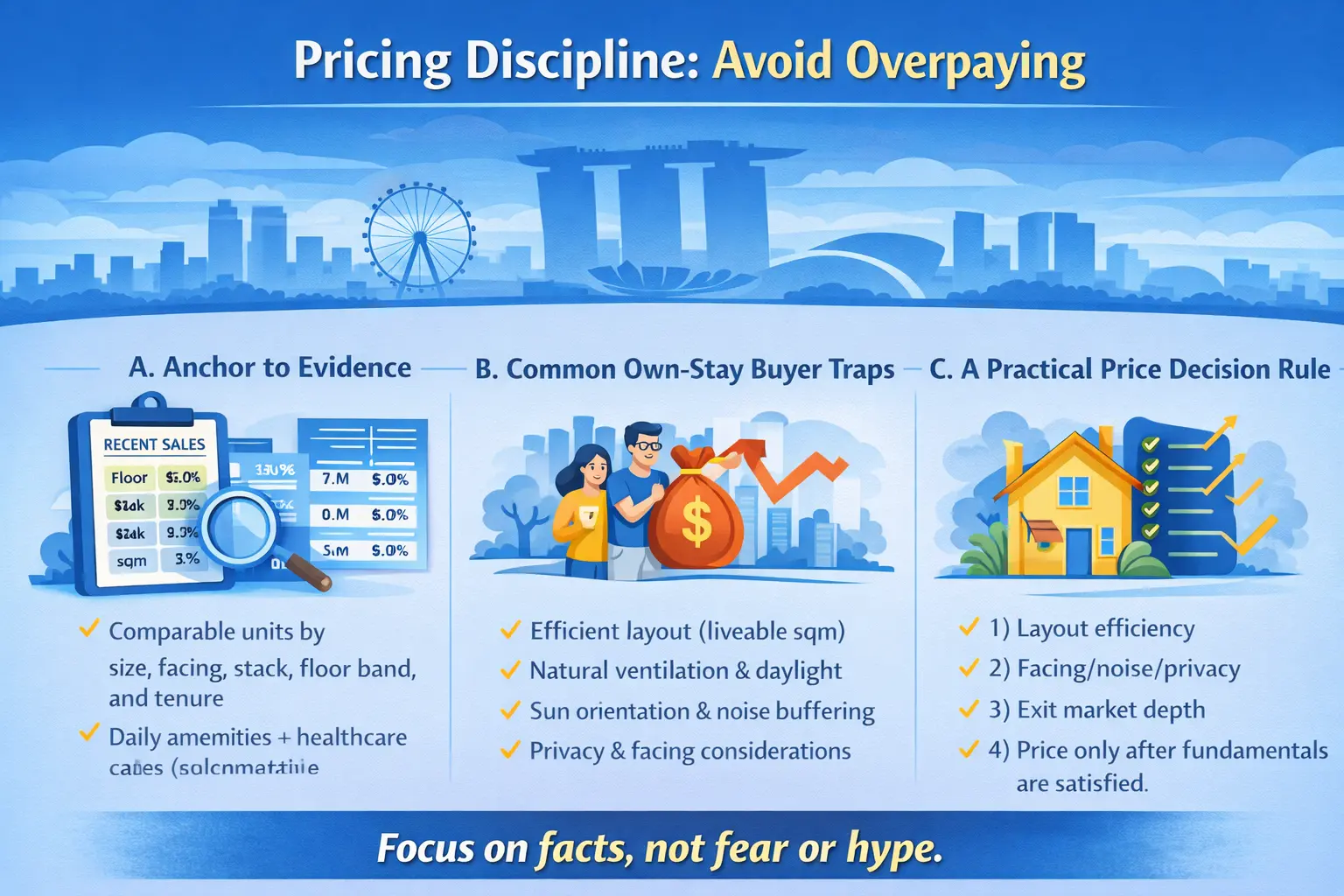

Unit Selection: What to Look Out For

For own stay, the unit itself matters deeply because it affects daily comfort. A buyer should avoid choosing only by price per square foot or a showflat impression.

Layout Efficiency

- Usable bedroom sizes

- Dining and living space flow

- Storage practicality

- Balcony size and usefulness

- Wasted corridor space

Daily Comfort

- Natural light and ventilation

- Afternoon sun exposure

- Noise from roads, MRT, schools or facilities

- Privacy from neighbouring blocks

- Lift access and refuse chute location

Future Use

- Family expansion

- Work-from-home needs

- Ageing parents or elderly-friendly layout

- Children’s schooling needs

- Possible future rental or resale appeal

Pricing: How Own-Stay Buyers Should Think

A beautiful home can still be financially risky if the entry price is too high. Buyers should review pricing with context, not emotion alone.

Compare Recent Transactions

Look at recent transactions in the same project, nearby projects and similar property types. Compare size, floor level, facing, age and condition.

Understand Price Gaps

A higher price may be justified by better location, view, floor level, layout, scarcity or project quality. But the reason must be clear.

Avoid Overstretching

Own-stay buyers should not depend on future capital appreciation to rescue an overcommitted purchase. The home must be sustainable from day one.

CEA-Safe Buyer Conduct and Agent Engagement

Buyers should work with registered property agents and understand the scope of representation clearly. A buyer’s agent should act professionally, explain relevant documents and avoid conflicts of interest.

Before Engaging an Agent

- Check that the salesperson is registered with CEA

- Clarify whether the agent represents you or another party

- Understand commission arrangements in writing

- Use CEA’s prescribed estate agency agreement where appropriate

- Ask the agent to explain relevant checklists and documents

Buyer Due Diligence

- Verify property facts and floor area

- Check tenure, title and restrictions where relevant

- Review financing before paying deposits

- Do not rely only on verbal promises

- Seek legal, tax or banking advice for complex cases

Official reference: Check if your property agent is registered with CEA.

Private Buyer Own-Stay Checklist

Before Viewing

- Set realistic budget range

- Check CPF OA and cash available

- Understand possible BSD and ABSD

- Review TDSR and LTV position

- Shortlist locations based on daily life needs

During Viewing

- Check layout efficiency

- Observe noise, sun and privacy

- Review maintenance condition

- Check lift, access and parking convenience

- Compare actual condition against asking price

Before Committing

- Confirm bank assessment

- Estimate total cash and CPF required

- Review legal documents carefully

- Stress-test monthly instalments

- Keep emergency reserves after completion

UProperty.sg Buyer Planning Tools

These tools support clearer, more responsible private property buying decisions.

Affordability Calculator

Estimate realistic buying capacity using income, CPF, cash and loan assumptions.TDSR Calculator

Check how total monthly debt obligations affect private property loan affordability.Loan-to-Value Calculator

Estimate possible loan limits based on property loan count, tenure and age factors.BSD & ABSD Calculator

Estimate buyer stamp duties and possible ABSD exposure based on buyer profile.CPF Usage Calculator

Understand how CPF OA usage may support or affect private property planning.Progressive Payment Calculator

Useful for new launch and EC buyers planning stage-by-stage payments.Holding Power Score

Stress-test whether you can hold the property beyond initial loan approval.HDB Upgrading Guide

For HDB owners planning to sell and move into private property.Sales Proceeds Calculator

Estimate net proceeds if your purchase depends on selling an existing property.Frequently Asked Questions

Is price per square foot the most important factor?

No. Price per square foot is useful, but own-stay buyers should also consider layout, liveability, location, maintenance cost, family needs, financing and future flexibility.

Should I buy new launch or resale for own stay?

New launch may suit buyers with more time and interest in newer facilities. Resale may suit buyers who need a home sooner and want to inspect the actual unit. The better choice depends on your budget, timeline and lifestyle needs.

Can I use CPF to buy private property?

CPF Ordinary Account savings may be used for eligible residential property purchases in Singapore, subject to CPF rules and withdrawal limits. Always check your own CPF position before committing.

Does loan approval mean I can comfortably afford the home?

Not necessarily. Loan approval is only one part of readiness. Buyers should also consider emergency reserves, interest-rate stress, CPF contribution changes, renovation costs and long-term household commitments.

Official References for Verification

Buy for Own Stay With Clarity, Not Pressure

A good private home is not only one that looks impressive today. It should fit your finances, lifestyle, family needs, loan position, CPF strategy and long-term holding power.

Professional and Regulatory Disclaimer

This article is provided for general educational and awareness purposes only. It does not constitute financial advice, legal advice, tax advice, CPF advice, HDB advice, banking advice, valuation advice, investment advice, or a recommendation to buy, sell, invest, upgrade or hold any property.

Property policies, CPF rules, stamp duties, loan requirements, eligibility conditions and market conditions may change. Buyers should verify all information with the relevant authorities and qualified professionals before making any commitment.

No representation is made that any property purchase will result in profit, capital appreciation, rental yield, loan approval, CPF eligibility, tax remission, successful resale, or suitability for every buyer. Past market performance is not indicative of future results.

Andrew Koh is a licensed real estate salesperson in Singapore. Any property-related discussion on this website is general in nature and does not take into account your full financial circumstances, objectives, needs or risk profile.